Kura Sushi is a dinky (~$540M market cap) sushi business that I have reported on for a little over one year. The US subsidiary is das kind (German for ‘the child’ because, why not) of a well-capitalised parent with over 450 stores in Japan. It’s a proof of concept venture in a new market, with a tried-and-tested business model, and a parent that provides ample liquidity to its fledging offspring. Sitting at 37 stores nationwide, and aspirations of 300+, it would be audacious to suggest that Kura alter the fabric of the US sushi market like Starbucks did with coffee, McDonalds’ did with obesity, or Subway did by somehow fooling people into believing a foot-long sub was enabling people to ‘eat fresh’. This non-franchised restaurant chain is less aspirational, but with good unit payback periods and a strong runway for growth, it has my interest piqued. That said, the current valuation does not have my mouth watering.

The migration from Japan → America, the backstory, the concept that makes the Kura experience unique, the technology, and just about everything else can be found in older memos I have shared below. Today’s memo serves as an update on the business, and my commentary.

For additional company-related commentary, please review my previous Kura Sushi memos (“KRUS: Kura’s Pricing Power”, KRUS: A 2022 Story, with a Price Tag”, “A Turnaround Story for Rotating Sushi”, “Kaitensushi (回転寿司)”.

Key Takeaways

• Enhanced AUVs: Commentary suggests that management believes pre-covid Average Unit Volumes ($3.5M) have the capacity to expand further than once imagined.

• Pricing Power: Kura has thus far managed to control costs in this inflationary environment through pricing events.

• Liquidity: Remains strong, boding well for the continued store expansion.

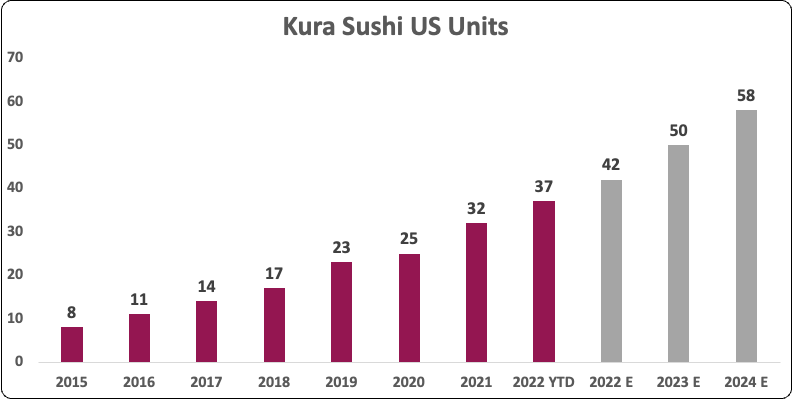

• Storecount: 37 stores now open, with a further 3-5 expected to be opened in Q4. This quarter, Kura entered a new state, Arizona, with 2 maiden stores.

• First Chief Marketing Officer: Kura hired their first CMO, Mark Finnegan. Hailing from a similar role at WaBa Grill, and serving various marketing leadership roles across the restaurant space (Wendy’s, IHOP, Pizza Hut). Bringing both IT and industry know-know, I later discuss how Finnegan’s arrival may influence the Kura Rewards business.

Kura Sushi’s Roll Continues

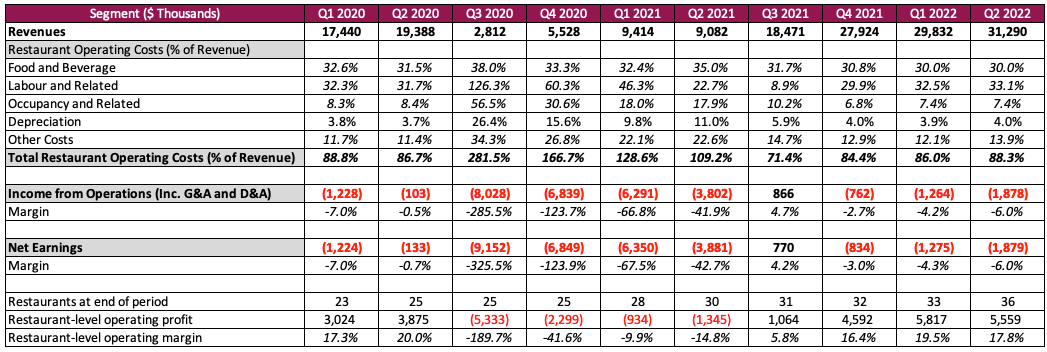

Having already risen from the ashes of covid in late-2021, the business put out another record revenue figure ($31.3M) in the second quarter, growing 5% sequentially.

Comparable restaurant sales, whilst impressive, are too warped (+182%) to really comment on. For a clearer perspective, this is ~13% comp growth from Q2 2020, and the first month of Q3 looks set to continue this promising trajectory with Uba acknowledging a record monthly sales total of $12.5M in March. Much can be said for how the fundamentals look today, and I will save that for further down the memo. All in all, nothing that really alters the investment case or the narrative; still fairly clean.

There were other, far more interesting, developments this quarter that warrant attention. The first of which being commentary on Kura’s long-term average unit volumes, and the second being Kura’s approach to pricing in inflationary environments.

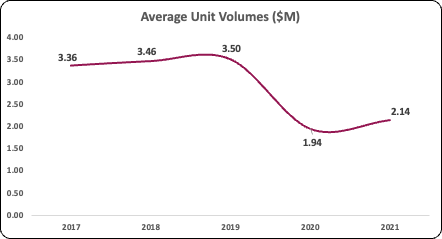

Potential for Stronger Average Unit Volumes (AUV)

A Kura unit takes approximately 4 to 5 months to acquire, build, and open. These units cost anywhere from $1.8M to $2.1M (ex-opening costs). Within 18 months (the timeframe in which a store is included in the AUV metric), a store was expected to generate an average of $3.5M in sales volumes per year, before covid. It’s a fairly solid payback period. Naturally, unit volumes plummeted in 2020/2021, and we will have to wait until Q4 to see how 2022 faired. I suspect AUVs return to upwards of $3.2M.

Store count has grown 61% (23→37) from 2019 until today, explaining why we are now witnessing explosive revenue momentum from $65M in revenue last year to an expected $135M this year. For almost two years, Kura has quietly been keeping its pedal to the floor with store expansion, and increasing CapEx when others were winding it down. The result, as the economy opens, is akin to releasing the pressure from a tightly-wound spring.

In this quarter’s earnings call, we learned that this strategy might have resulted in a serendipitous upside for AUVs with management remarking “we believe that the units from our fiscal ’22 details [new stores] have the opportunity to exceed historical AUVs.” Meaning, to exceed $3.5M. This likely won’t contribute to AUV levels until later in 2023, but management spoke about how there is scope to expand AUVs more broadly across the portfolio; citing the supply of prime real estate as a leading cause when other buyers were winding down CapEx.

“A lot of this is driven by the strategy we’ve taken in 2020 and 2021 in terms of unit growth, while pretty much every other restaurant company was totalling up and limiting their CapEx costs, we felt that this was a huge opportunity in terms of capturing prime real estate that might have been otherwise inaccessible or more difficult for us to access. And we’re extremely pleased to see that, that strategy has paid off, and the units are as productive as we’d hope they’d be.”

How sustainable this is going forward, when buyers presumably return, I can’t be sure. Talk is cheap, but prime real estate oft isn’t, so we’ll see.

We Don’t Like to Drive Margins Through Pricing

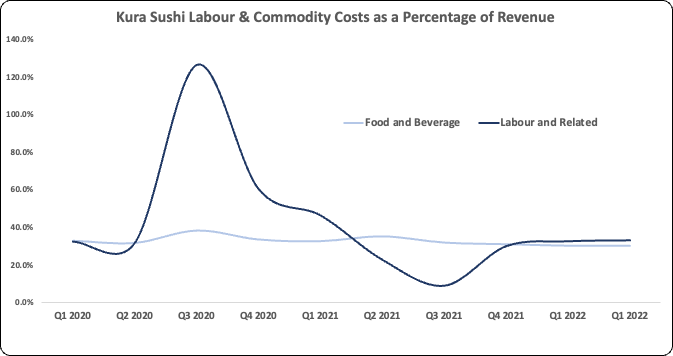

After taking a small pricing event last September, Kura enacted another in March (~1.8%) to offset an expected 1.25% increase in labour costs through minimum wage increases and ~0.8% in commodity inflation (as a percentage of sales). Last year’s pricing event went down without a hitch, per plate consumption remains greater than pre-covid levels, and it’s quite likely this event has immaterial consequences. With a wide variety of menu items and proteins, as well as an already low-cost per plate pricing, the consumer absorbs the cost without much thought, allowing Kura to keep its COGS under control. Commodity costs as a percentage of sales sit at 30% (unchanged from Q1), down 150bps from Q2 2020. I find it impressive that Kura has reduced food & beverage costs from pre-covid levels, considering the environment we are currently in.

Labour expense, on the other hand, currently sits at 33%, up ~140bps from Q2 2020. Not yet out of control by any means, there are longer-term initiatives to offset labour inflation. With touch panel ordering now in 22 stores (expected in all by the end of the year), and robot servers (discussed in “KRUS: Kura’s Pricing Power”) now in 15 more stores (20 in total), Uba cited the potential for “robot servers to deliver labour savings in the future”. It doesn’t require much imagination to see how automating the tasks of 1-3 servers per store can create savings. No update on the quantification of these initiatives (with respect to table turnover times), but Uba did comment that the 2 goals here are to increase sales (via faster turnaround) and to eventually reduce labour cost as a % of sales.

I wanted to share a quote from Uba, which I found insightful. When asked why Kura was not hiking prices in the mid to high single digits, like their peers, Uba responded as follows:

“We don’t like to drive margins through pricing. What we know is that delivering a great value has always been core to our brand. And in spite of the pricing that we’re taking, the purchasing power of the rest of the sushi industry being so fragmented is just not nearly on the same scale as we are. And so the mom-and-pops are having to take far more price than we are. And so in spite of the pricing that we’re taking, value delta continues to grow. So, I think we’re pretty happy with our position right now.”

The value delta comment reminded me of Costco, albeit they are not entirely the same. Many stress that the ability to raise prices is a sign of ‘pricing power’. Contrary to popular belief, it’s actually the ability to raise prices when your competitors dare raise theirs. Alternatively, the ability to not raise prices when your competitors feel they have to is another advantage. In this case, Kura is raising prices considerably less than their peers. Thus, pricing power is more so related to the ability to control when and how you raise prices, if at all, and having the benefit of (a) not losing customers in pricing events and; (b) stealing customers, or maintaining a low-cost stronghold when competitors have to raise.

Put more succinctly, Todd Wenning of Ensemble Capital would say; “pricing power is the ability to confidently set prices at times when your competitors need to have a prayer session before they would consider raising theirs.”

I have spoken in the past about how Kura’s light protein per plate, extensive commodity basket, low cost, and non-reliance on particular items, allows them to shield themselves from inflation, raise prices, and not antagonise the consumer. I still believe that to be the case.

Stores and Rewards

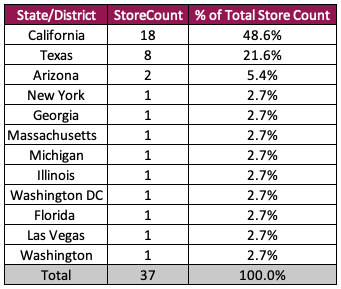

As announced during Q1, Kura opened two units in Arizona, their 11th market in the States, as well as one additional store in Texas. Following the quarter, an additional store was opened in Watertown, Massachusetts, their 12th market, for a total of 5 stores opening this year.

Going forward, management expects a ~50/50 split of store openings between new and existing markets. With 5 units currently under construction, it is expected the remainder of 2022’s new units be opened throughout Q4.

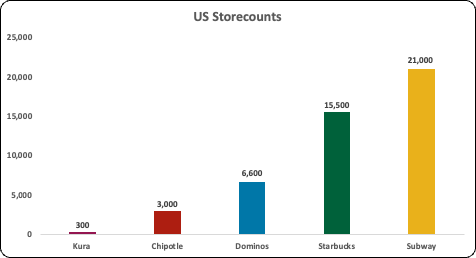

With the cadence of new units humming along nicely, and covid seemingly in the rear-view mirror, I think back to Uba’s words in the Q4 2021 call, where he expressed intent to “commission a new whitespace study once COVID is finally behind us”, after admitting he feels Kura’s “whitespace potential is larger than ever due to pandemic-driven restaurant closures”. At present, that whitespace is proposed to be ~300 stores nationwide. Merely as a means of illustration (because America’s appetite for burgers, coffee, pizza, Mexican food, and footlongs is incredible), the below table shows it’s not alien to imagine an America with a sushi chain that amounts to more than 300 stores.

The most glaring flaw in this comparison is that Kura is not a chain optimised for franchising, nor is it an establishment equipped for ‘on the go’ experiences. Whilst off-premise sales gained momentum during in-house dining restrictions, they have trickled back down to mid-single digits as a percentage of revenue, albeit considerably higher than pre-covid levels of ~1%.

Is this something Kura are optimising for? Sadly, no. After passing commentary last year about introducing off-premise architecture (pick-up windows) in construction planning, it’s still seen as “gravy”; a nice to have, with unit growth being the overarching goal.

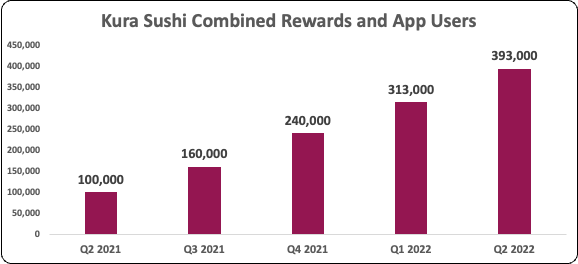

Lastly, before ducking into the financials, Kura added an incremental 80,000 Rewards members in Q2, totalling 393,000.

With a new CMO in place, it appears one of his first tasks, will be to improve the functionality, usefulness, and hopefully the gamification, of the Kura Rewards app. With the quirky, already gamified, Kura experience this rewards program is screaming for a playful and engaging rebrand.

“As a preview of things to come, any project is the development of the next stage of our rewards program. In past earnings call, we had mentioned that the true potential of our rewards program will only be unlocked once we have the ability to leverage guest data. And with Mark, we have the perfect person to spearhead this effort.”

Financials

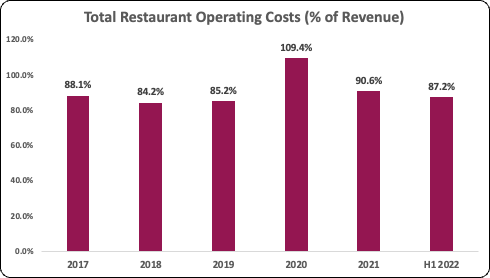

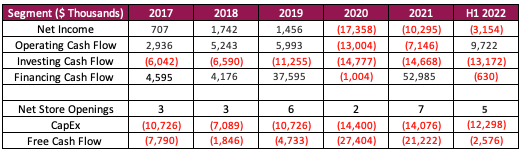

On track to more than 2x revenues in 2022, Kura is expected to continue breaking sales records for the remainder of the year. But perhaps most importantly, restaurant operating costs are normalising after reporting negative gross margins in 2020.

You will note (in the below table) that in Q3 2021, restaurant-level operating costs reached lows of 71% before hitting the mid-80s the following quarter. Merely a matter of catch-up at play there, during a time when sales rebounded faster than costs. Typical norms for Kura are in the mid-80s.

As discussed earlier, Kura’s two pricing events (September, and now March) have, and will, assist in offsetting this inflationary cost environment we find ourselves in. As for when profitability comes into play, I have no superior insight. The parent company, Kura Sushi Japan, operates with a gross margin in the mid-40s, with operating margins in the mid-single digits on a base of ~$1.2B in annual revenue. It is my opinion that Kura US’ payback period is reasonably attractive and that economies of scale will afford Kura US margin expansion over time.

Balance Sheet

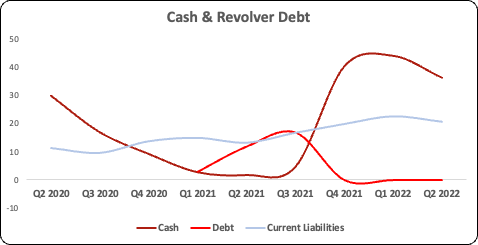

Covid took place just as Kura had burned down the last of its cash reserve from the 2019 IPO. Thankfully, the parent Co was on hand to provide liquidity with a $45M revolver facility, of which Kura utilised $17M before a near-perfect execution of stock, netting the company $47.1M and allowing them to prudently pay down the credit facility. Over the past three months, Kura has burned through ~$8M in cash but still remains in a comfortable position with $36.4M in cash and equivalents on the books for a cash ratio of 1.75x.

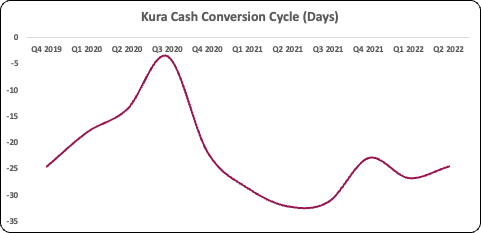

Assuming Kura build anywhere between 8-10 additional stores (5 of which are under construction and expected to roll out in Q4) over the NTM, then that should eat up between $18M to $23M in capital before the addition of opening expenses, alcohol licenses, hiring, and so forth. Kura has also generated $12.2M in operating cash flow over the last three quarters. Whilst this is an amicable runway of cash burn, it won’t be long before questions are raised over Kura’s liquidity once again. The safety net, in this case, is that $45M revolver that sits untapped. One last point, and I consider this to be an important one when we are musing about liquidity; is Kura’s cash conversion circle is negative.

That is, they buy inventory from suppliers, and collect revenue on the sale of said inventory before they pay creditors. Whilst Kura typically have up to 30 days to pay their vendors for inventory, sales are collected from the customer immediately (cash) or within a few days (credit card); thus giving Kura an attractive amount of leverage.

Cash Flow Statement

Cash flows are in a markedly better place than one year ago.

Echoing my comments from previous memos, free cash flow is not a priority at this stage. One would hope that the bulk of Kura’s operating cash flow is allocated to CapEx for new units.

What could de-rail this business?

Much of the substack-arazzi (myself included) spend an infinite amount of time posturing on fundamental outlook and trends. Seldom do investors talk about what can go wrong. Besides paying a silly multiple for Kura, here are a few figments of my bear case.

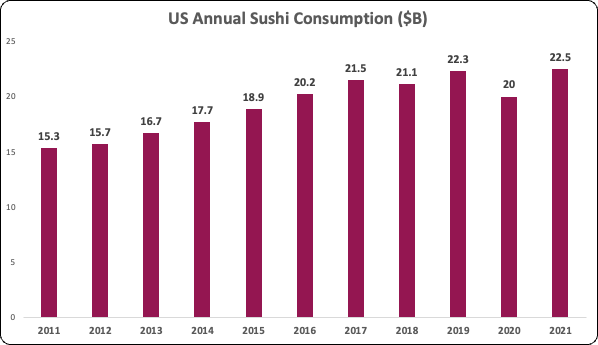

Sushi Isn’t American: Jestingly, because neither is pizza, chicken wings, or a number of other staples of popular fast-food chains in the States. What is a recurring theme amongst these chains is they are “Americanized”. Despite sushi’s growing appeal in the states, the $22.5B annual consumption in 2021 baulks in comparison to the $272B that US consumers spent on fast food in the same year.

Kura does share the low-cost, quick dining, experience as some fast food joints, so it may appeal to consumers’ wallets, as well as growing health concerns, but that is yet to be seen.

Controlled Ownership: Over 50% of Kura’s shares, and over 80% of the voting power are controlled by the parent entity. Despite the US subsidiary finding its footing in the US, any manner of reasons could result in the Japanese parent closing down Kura US for matters of liquidity, or other. Kura US rely heavily on their parent for branding and IP rights, supplier relationships (of which two suppliers accounted for 85% of all food costs in 2021) and liquidity.

State Concentration: Ideally not a LT threat, but Kura’s 70% concentration across CA and TX puts them at the mercy of state-level policy change. This composition has fallen from 85% in the last year, but a reliance of California, in particular, could be troublesome should any labour, rental/lease, policies change.

Liquidity: Whilst the revolving credit facility is a nice safety net for Kura, it doesn’t appear likely the business can self-sustain until the rate of store openings slows down. Naturally, this contradicts their ambitious growth goals. Over time the impact of 10 new stores in a given year will become relatively smaller, but for now, store openings per unit have a material impact on revenue growth. There can be no assurances that (a) Kura can extend its $45M revolver, (b) Kura can raise capital in future market environments, and (c) Kura can self-fund their operations should liquidity dry up.

Inflation: At this stage in their life cycle, without the benefits of economies of scale, Kura’s margins are razor-thin (gross) or non-present (EBIT). Terry Smith oft remarks that the best buffer for inflation is a strong gross margin. Whilst Kura have done well in offsetting inflation thus far, a strong gross margin is not something they possess.

Concluding Remarks

The quarter was concluded with a reaffirmation of guidance; total revenues of $135M (mid-range) by year-end, G&A expenses to be ~17% of sales (a one-time distortion discussed in “A 2022 Story, with a Price Tag”), and the opening of 8-10 stores, of which 5 are already open.

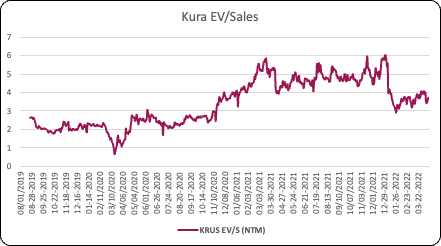

Looking ahead, analyst estimates are in line with 2022 revenue guidance, followed by $179M (2023) and $222M (2024) in subsequent years, with minor EBIT positivity expected in 2023 (3.5% margin expected in 2024). On that basis, Kura trades at an EV/Sales NTM of 3.4x. Whilst down considerably from the 6.1x levels portrayed in December of 2021, the current valuation weights each of Kura’s stores at ~$14.6M, or about 4.2x their pre-covid expected AUVs.

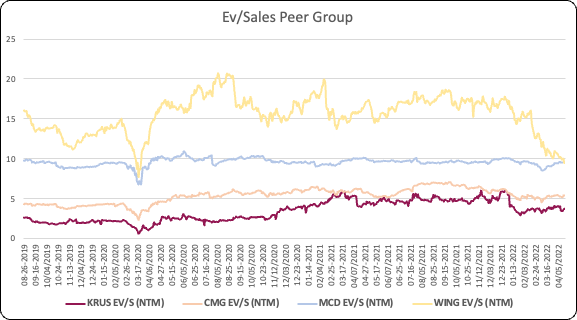

Thinking back to when I first acquired a stake, in May 2021, the value per store was closer to $10.5M, which in my opinion was still rich. One can look to Kura’s “peers” (I use that term very loosely) and see it trades considerably lower on a NTM EV/Sales basis, but none of these alternate businesses is as fragile as Kura, or as unproven with respect to product-market fit, and each possesses far greater resources, margins, economies of scale, and management.

Investors typically pay a premium for ‘quality’, and I would not be so ignorant to suggest Kura is quality quite yet. What’s more, if you were to compare Kura against a backdrop of more traditional measures (EBIT, Cash Flow, EBITDA, etc), you would find it doesn’t look so ‘cheap’ compared to peers. Whilst I am more than content to continue owning this business, I haven’t found an attractive point of re-entry just yet, being mindful that I want to keep this 2.5% position in the lower rungs of my portfolio for now.

Thanks for reading.